a Metropolis for every asset class

photons, payments, a $1.5B take-private, and a recognition layer underneath the world.

buildings that work

I’ve always been fascinated by buildings. Not the architecture exactly, but the engineering of how they work. The question that nags at you in a hotel lobby at 8am is what the great ones do that the others don’t. I’ve been thinking about it for years across airports, train stations, hotels, museums, stadiums, hospitals. The answer is never quite the floor plan, never quite the technology, never quite the staff. It’s something underneath all of them.

Take airports. Singapore Changi feels like infrastructure designed by people who care, where moving through the building is itself part of the product. Istanbul’s new airport is the same way. Compare that to New York JFK, which feels like several different cities glued together with concrete, or Miami, where the signage actively wants you to miss your flight. The difference between them isn’t square footage or architect or terminal age. It’s the layer underneath. Hotels, warehouses, and whole cities are the same.

Around a year ago I heard about a company called Metropolis for the first time. A parking software startup founded in 2017 in Los Angeles, in the sixth year of its existence, had just bought out a publicly traded, 100-year-old giant SP Plus Corporation for $1.5 billion. I’ve repeated that line to friends and strangers more times than I can count, and I keep coming back to the same thought: there should be a Metropolis for every asset class.

This piece is me trying to debug that fascination. What is Metropolis actually doing under the hood? Why did it work? And what does the future look like in an increasingly self-driving cityscape? Let’s dive in.

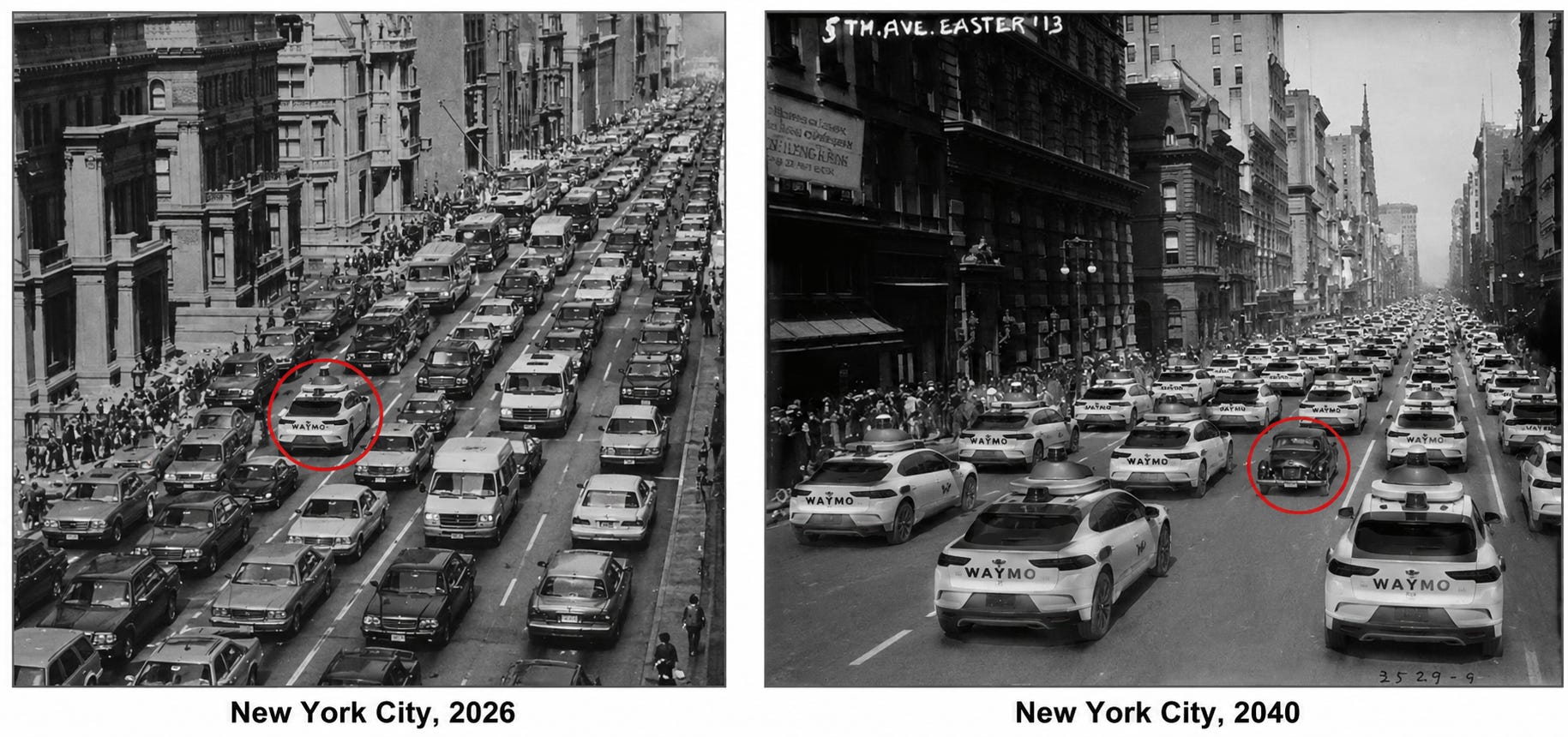

Thirteen years. That’s how long it took to change what New York City actually ran on. The lone horse in the 1913 photo is the tell, not because the horse is rare but because the cars aren’t. Henry Ford launched the Model T in 1908, and within five years the city had built out curbs, paved high-speed grids, traffic signals, parking, and gas stations. None of that existed in 1900. By 1913 the whole city ran on it. The thing about a shift like this is that you can’t see it from inside. There was no day where anyone announced the change. It just kept happening, until one day you looked around and the horse was the anomaly. We’re in the middle of the next one.

cute startup, come back in 30 years

Metropolis was founded in 2017 in Los Angeles by Alex Israel and a small team of co-founders. Israel grew up on LA’s west side, went to Crossroads School for the Arts and Sciences in Santa Monica (alumni include Maya Rudolph and Jonah Hill), studied business at the University of Puget Sound, then got an MFA in producing from the American Film Institute. He worked briefly at MTV/Viacom and at Walt Disney before tech.

Israel’s first company was ParkMe, founded in 2009 with his lifelong best friend Sam Friedman after they missed a movie because they couldn’t find parking. They sold it to Inrix in 2015 for cash and stock.

The early Metropolis product was good. The technology worked, and the unit economics held up at the pilot garages they did manage to deploy. The problem was distribution. Institutional real estate owners (REITs, pension funds, hospitals, airports, municipalities) would not deploy an AI startup’s tech across thousands of garages. Asset owners didn’t want to underwrite the technology risk. The industry’s reception, per Israel:

“Cute startup. Come back in 30 years.”

The pivot was to acquire the operators instead of selling to them. Israel calls this the Growth Buyout. Every traditional rollup playbook runs on cost cuts: buy the operator, strip staff, run the asset cheaper, expand the multiple. Israel’s framing on The Split with Turner Novak is the opposite: “Cost synergy doesn’t create durable growth. We focus on revenue synergies.” Buy the operator, leave the operating model largely alone, and layer the AI on top to drive new revenue. We’ll come back to whether that framing survives the operating evidence.

drive in, drive out

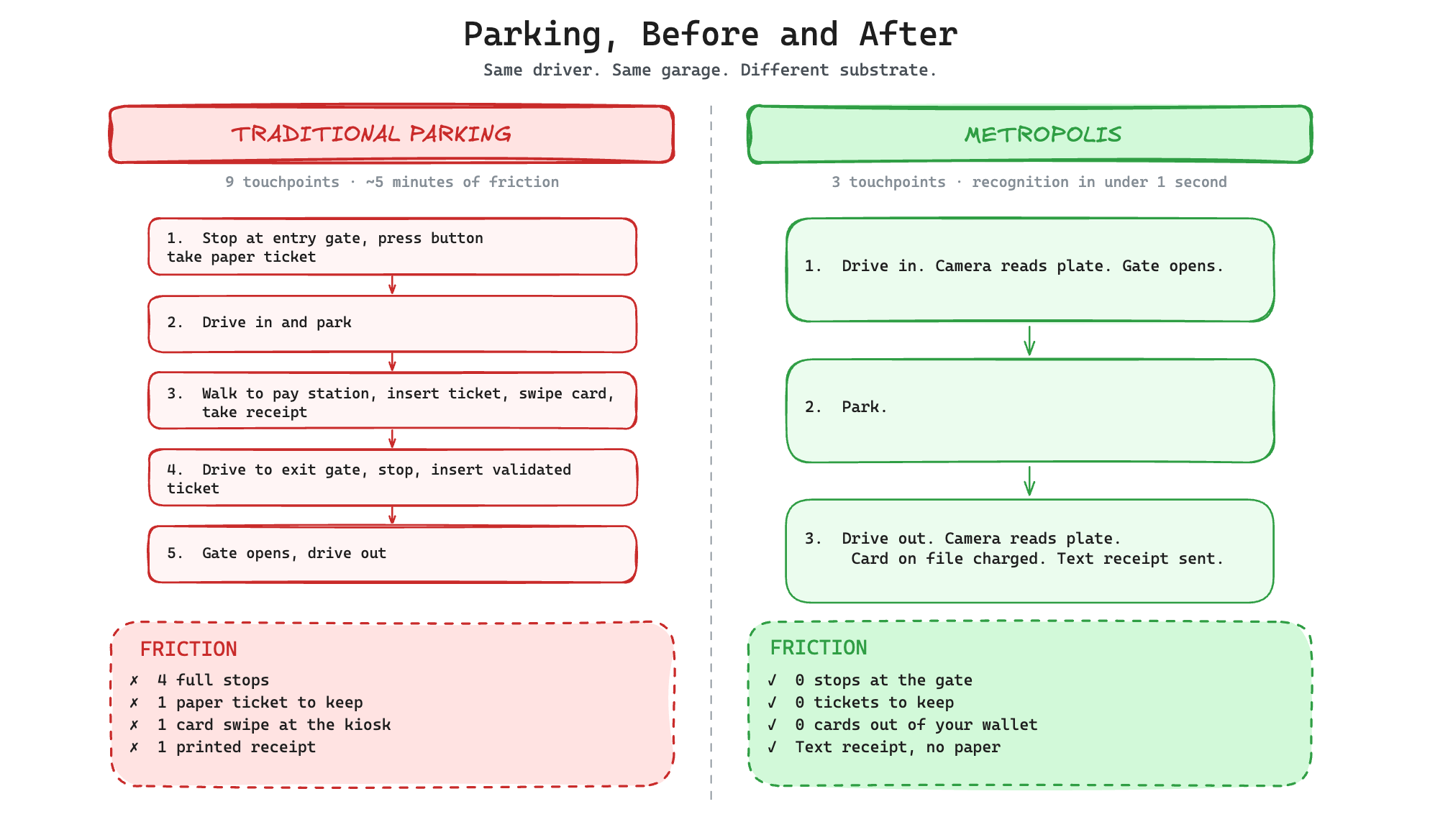

What it feels like at a Metropolis garage on the first visit is roughly this. You pull up, the camera reads your plate, the gate opens, you drive in, and when you leave you get a text receipt. No ticket. No kiosk. No app required. On the next visit it’s already memorized your car, even at a different garage in a different city.

The reason this matters is the layer underneath. Metropolis isn’t really selling parking. The company puts it directly on the homepage: “We’re making the world more intelligent with an AI-driven recognition platform that understands, adapts and responds in real time. Our platform is the foundation for a future where routine interactions are smoother and smarter.” That’s the actual product. A recognition layer, with parking as the wedge.

The license plate is the cleanest first identity credential because it’s the only one that already exists on every car, regulated and standardized by every government, requiring no enrollment and no app trust. Once the cameras and gates and payment rails are in place, the same sensing extends to anything that wants the same one-touch experience. In Israel’s words:

“It’s about being recognized everywhere you go.”

photons to payments

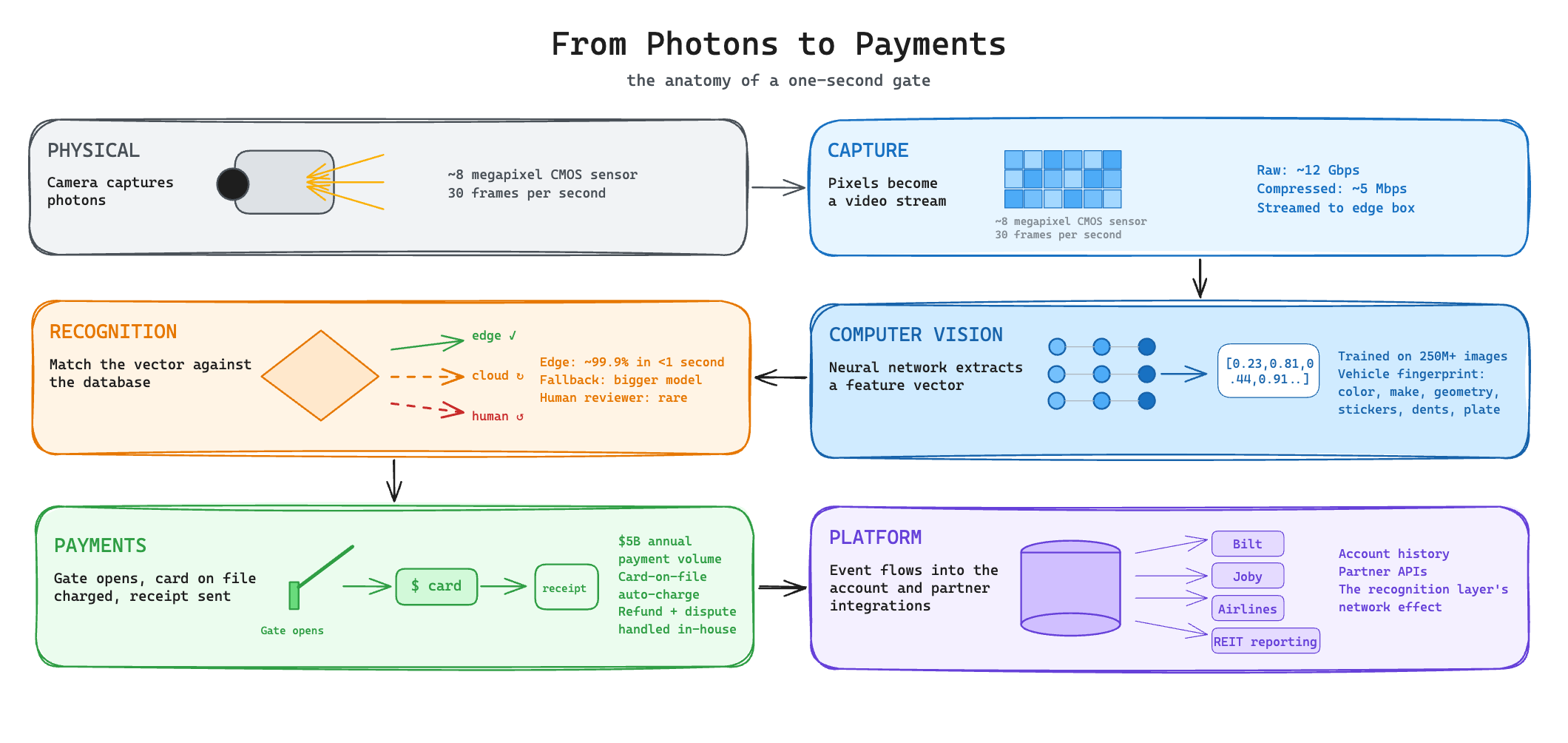

If you’ve never opened up the question of how a computer recognizes a car, the short answer is that it doesn’t, not the way a person does. A camera doesn’t see a car, it sees photons hitting a grid of light-sensitive cells, and the whole stack on top of that is the engineering work of converting that physical signal into a decision.

A digital camera is a grid of CMOS image sensors that count photons during a fraction of a second. The output is a two-dimensional array of numbers, three channels deep for color. At 30 frames per second, that’s a few million numbers per frame, compressed and routed somewhere they can be processed.

Computer vision is the engineering discipline of pulling structured information out of those arrays. Hand-written rules don’t survive the real world (different angles, lighting, occlusion, weather), but a neural network trained on millions of labeled examples can extract features directly from the pixels. The output isn’t a label like “car” or “truck.” It’s a vector of a few thousand numbers that encodes the image’s content relative to the training set. Two images of the same vehicle produce vectors close together. Two different vehicles produce vectors far apart. The rest of the stack is distance comparisons.

Recognition is the act of asking, “have I seen this vector before?” Metropolis extracts the vector at the edge, on a purpose-built compute box inside the garage. A match against the local database resolves in under a second. An unclear match (bad angle, dirt on the plate) routes to a more expensive cloud reidentification model, and the residual goes to a human reviewer. What makes the stack different from usual ALPR is what gets trained. Most plate readers do OCR on the text, which is brittle in the real world. Metropolis trains on the whole vehicle: color, make, geometry, stickers, dents. The training set is more than 250 million images.

Recognition is only the first step. Once the vehicle is identified, the money still has to move, and Metropolis runs the payments rail itself: card-on-file, automatic charging at exit, receipt delivery, refund handling, dispute mechanics. The company processes over $5 billion in annual payment volume across the network. Recognition without payments is identification, recognition with payments is a transaction, and the two together are the product.

Sitting on top of both is the platform layer. Every event flows into a customer account that holds vehicle records, payment methods, contract terms with operator-clients, partner integrations (Bilt rewards, Joby vertiport bookings, airline check-in via Bags VIP), and the historical record that makes future recognitions cheaper. The world model is a software construct, a continuous representation of who is where, what they’ve done before, and what they’re authorized to do next.

buying the EBITDA

Metropolis’ first acquisition was Premier Parking in 2022, a Nashville-based operator with roughly 450 garages across 20+ cities. By the time Metropolis bought it, Premier had been through five years of PE ownership under River Associates.

Israel describes Premier as the unit-economic proof point that made everything afterward possible. The headline numbers were “a little north of $120 million” for “around $10 to $12 million of EBITDA,” with gross profit doubling “relatively overnight” after the CV stack went live.

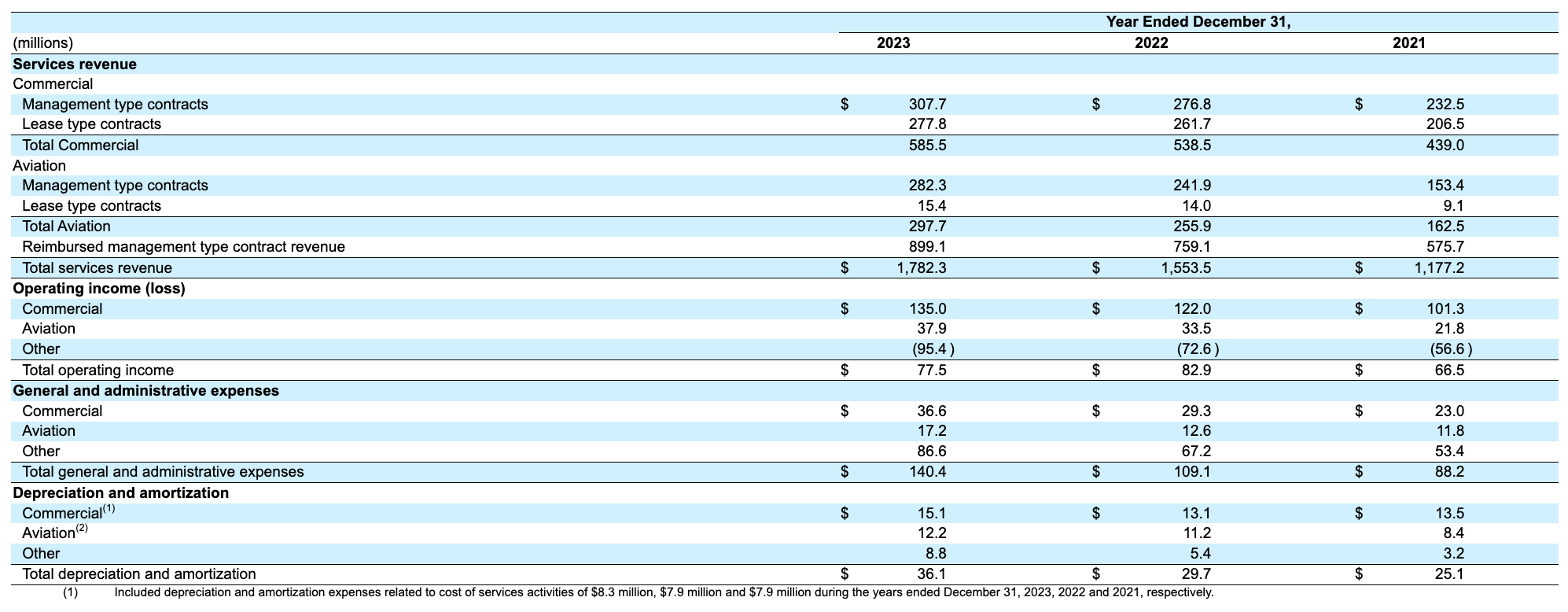

Eighteen months later they did it at thirty times the scale. The $1.5 billion SP Plus take-private was the largest VC-backed M&A deal of 2024. Metropolis got over 4K commercial locations, 159 airports, 19K+ employees, and $1.78 billion services revenue against $110 million EBITDA.

Two contract types underwrote that revenue. Per SP’s 2023 10K, Management contracts (fee-based, client owns the gross receipts) were 88% of locations but only about half of Commercial revenue. Lease contracts (SP+ pays a base rent plus a percentage, collects the receipts itself, bears the operating costs) were 12% of locations but the other half, about 14x more revenue per location. Management contracts ran one to three years and lease contracts three to ten, but most were cancellable on as little as 30 days notice without cause.

Prior to the acquisition, SP+ had been racing to build the digital layer themselves. They had their own tech suite (Sphere), had bought their own frictionless-parking software (DiVRT) a year before the Metropolis deal was even announced, and ran an engineering shop in India. Metropolis bought a half-digitized business and finished the job.

In October 2023, Metropolis raised $1.7 billion of debt and equity to take SP+ private. The interesting move came a year later. By November 2025, SP+ had been on the company’s consolidated books long enough for the cash flow to show, and Metropolis used that as collateral to raise a different kind of capital: $1.1 billion in a Term Loan B, paired with $500 million in Series D equity led by LionTree at a $5 billion valuation.

Banks don’t normally underwrite venture-backed companies. By owning a 100-year-old business that actually generates EBITDA, Metropolis made itself loanable. The lead investor signals where this is headed. LionTree is a merchant bank, not a typical growth shop, and the partner running the deal, Ramin Arani, spent 26 years at Fidelity. This could suggest that Metropolis was being priced like a future public company. In May 2026, Israel himself acknowledged the IPO question in Fortune:

“It would be wonderful.”

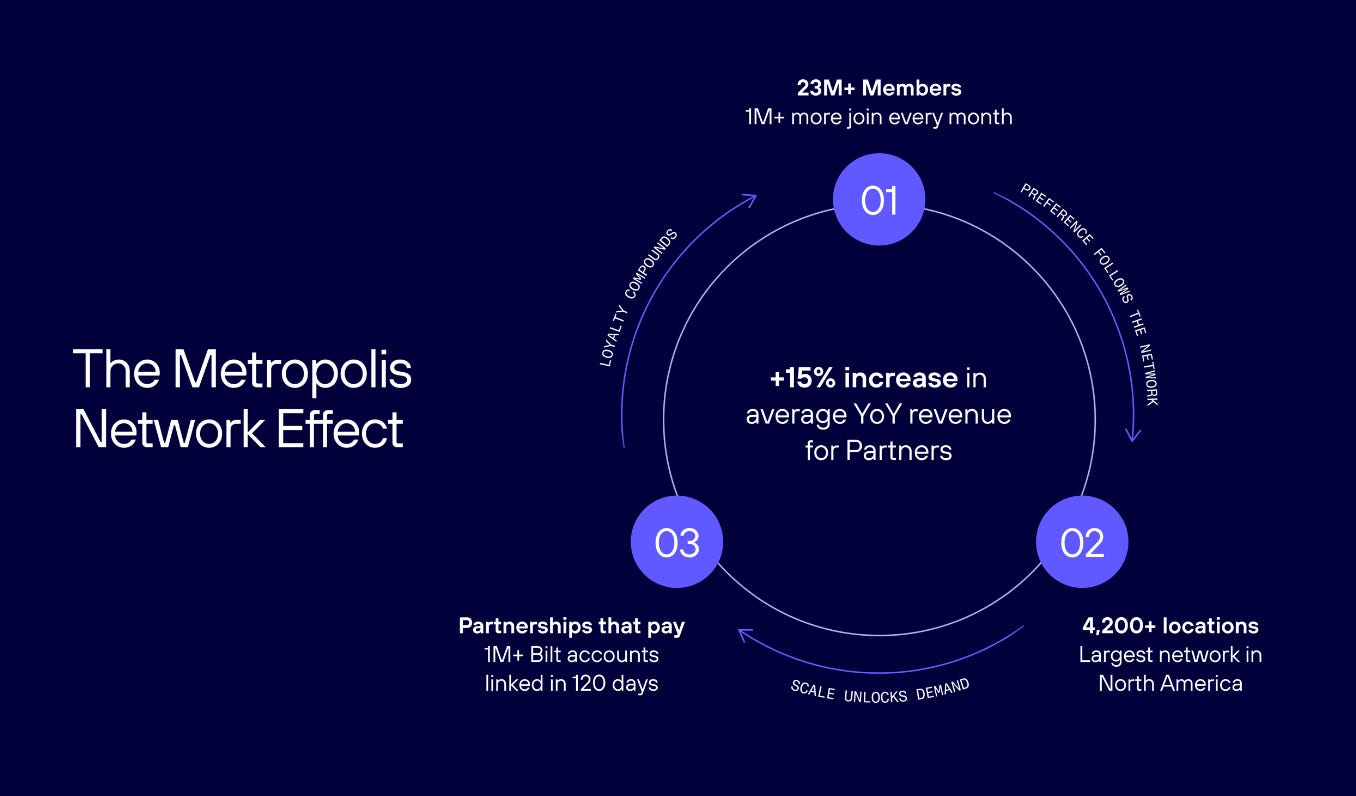

What makes that valuation defensible is that Metropolis is a compounding network. 23 million members, 4.2K locations, 18 million vehicle events a month, with partners reporting an average 15% year-over-year revenue lift after joining. Each new member makes the network more attractive to partners, and each new partner makes the network more valuable to members.

the cost of scale

The harder, less-discussed part is installation. Retrofitting thousands of physical locations across every metro area in North America, each with different gate hardware, power layouts, ownership structures, municipal regulations, union jurisdictions, and bandwidth availability, is a fundamentally different problem from training a computer vision model. The hardware that runs all of this is vertically integrated.

Metropolis uses proprietary camera systems designed, manufactured, deployed and maintained in-house, weather-hardened for direct sunlight, deep shadow, and high-angle approaches. Each garage gets its own purpose-built compute box, its own power supply, its own bonded fiber link if existing bandwidth doesn’t cut it.

Metropolis inherited roughly 19,900 employees from SP+, most of them attendants, shuttle drivers, baggage handlers, and valets running the existing operations day-to-day. The retrofit motion itself is a separate workstream, and the company doesn’t disclose how much of it is in-house versus contracted.

Every install at scale also imports the legacy operator behavior. In January 2026, Metropolis settled with the Tennessee Attorney General for $8.75 million over deceptive pricing, surprise fees, government-mimicking violation notices, and blocked refunds, after more than 300 consumer complaints over two years. A separate federal class action under the Driver’s Privacy Protection Act is open over how Metropolis accesses motor vehicle records to issue parking notices, a mechanic that traces directly to Roker, the citation-enforcement software SP+ acquired in 2023 and that Metropolis inherited with the deal.

Reddit reads a little worse than the Fortune coverage. From r/cincinnati in December 2025, a customer paid $22 online for parking at the Music Hall lot, got a paid confirmation, then received a mailed bill for $78 a month later. From r/kansascity in September 2024, paid $2.99 by QR code, charged correctly, then received a “violation notice” for $53.25 weeks later. From r/LosAngeles in February 2025, a driver drove 90 seconds into a Hollywood lot to turn around and was billed for 48+ hours at max rate.

Some of this is the cost of switching — integrating a 20K-person workforce and a 4K-location contract book into a single CV and payments stack was never going to happen cleanly, and the friction shows up first at the customer-facing edges. In the long run, most likely Metropolis cleans most of this up. The recognition layer only works if customers trust it, and the company’s incentives all run in the direction of getting that right.

three acts

Autonomous driving is doing to real estate values what Uber did 15 years ago, removing the friction of the commute, pulling location values outward, reshaping what “near” and “far” actually mean.

The Waymo in the 2026 photo above is this era’s version of the lone horse on Fifth Avenue in 1900, easy to miss in the moment, but definitive of the next decade in hindsight. The cars will drive themselves in, they’ll drive themselves back out, and somebody will be operating the gate they pass through in both directions.

In a self-driving world, the customer is the car itself. It still has to be identified at the gate, billed for whatever it did inside, and routed somewhere when it’s done — to charge, clean, or wait between rides. The parking economy (selling spaces by the hour) may shrink, but the recognition and payment layer underneath will get used even more.

The history of Metropolis reads in three acts. Act One was building the recognition layer. Act Two was becoming the parking company. Act Three is what we’re watching right now: Metropolis becoming the infrastructure for AVs and adjacent verticals.

Metropolis homepage lists some of Act Three’s verticals directly:

Effortless fueling: “Pull up to a gas station or EV charging point. No fumbling for cards, no apps to open. Just drive in, fill up and drive out.”

Intuitive retail: “Step into stores where checkouts are effortless, lines are a distant memory and recommendations are personalized.”

Connected communities: “From drive-thrus that remember your order to car washes that activate as you approach, our technology makes infrastructure recognize and react to your presence.” Same recognition layer, different rectangles of real estate.

The same shape exists across other real estate asset classes. Lineage Logistics rolled up the cold-chain warehouse industry, layered automation and robotics on top, and IPO’d in 2024 at $19 billion. Wander is doing the same for short-term rentals, owning and branding the homes themselves rather than running a marketplace. HATCo, the healthcare arm of General Catalyst, bought out a whole hospital system specifically to deploy AI infrastructure that is 100x harder to sell through normal procurement.

Once you start looking for the pattern, the list of underbuilt categories keeps growing: self-storage, marinas, stadiums, office, agriculture. The next decade of real estate belongs to the operators willing to consolidate the asset and digitize it at the same time. There’s a Metropolis waiting to be founded in every one of these categories.

I am excited for a future that feels more like Changi than JFK. Buildings that work and buildings that don’t have always had something underneath them deciding which they were going to be. Metropolis is betting they can be the company building that something, garage by garage, until one day you look around and the transition is over.

Thank you for reading!

— E